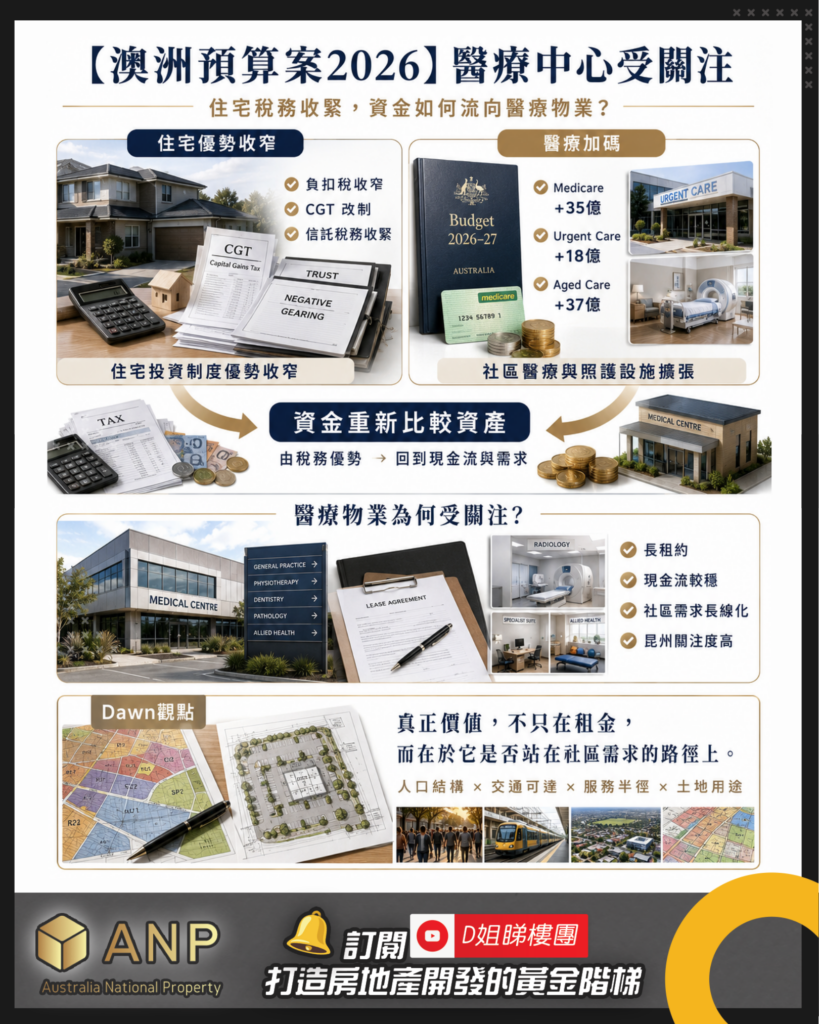

One of the most noteworthy changes in the property market following the release of the 2026 Australian Federal Budget is the renewed focus on medical centers and healthcare properties. While residential investment faces tax system adjustments, commercial properties are returning to the fundamentals of cash flow, leases, and usage requirements. In this repricing process, the reason medical centers have broken through is not simply due to the old adage of "doctor tenants providing stability," but rather because it involves an aging population, the expansion of community healthcare, the restructuring of care services, and the redrawing of urban living boundaries.

This budget places significant emphasis on healthcare and care. Medicare receives an additional $3.5 billion to increase bulk-billing facilities, reduce out-of-pocket healthcare costs for some seniors, and improve healthcare services for Indigenous peoples. The Pharmaceutical Benefits Scheme (PBS) receives an additional $6.5 billion to support medications for cystic fibrosis, chronic kidney disease, and various cancers. Aged care also receives an additional $3.7 billion, with a target of adding 5,000 beds annually. Regarding the urgent care clinic network, which is more directly linked to commercial properties, the government invests $1.8 billion to make Medicare Urgent Care Clinics permanent, increasing the number of clinics nationwide to 137. Public hospitals receive an additional $25 billion, bringing the total to $220.3 billion over five years. An additional $11.4 billion in bulk-billing incentives aims to ensure that nine out of ten GP visits are bulk-billed by 2030.

These figures, while ostensibly public spending, signal a shift in urban healthcare services from a centralized to a community-based model. Large hospitals remain the core of the system, but more routine medical care, emergency triage, chronic disease management, rehabilitation, elderly care, and allied health services will increasingly need to be available within residents' living radius. The value of medical centers lies precisely in this turning point, transforming from "a rental property" into "community infrastructure."

ANP urban planner Dawn believes that the key to judging the value of a medical center lies not in its name, but in whether it is situated at the heart of the community's needs. Good healthcare properties must have a sufficient population hinterland to support them: the proportion of elderly residents, family size, chronic disease needs, public transportation, parking arrangements, drop-off areas, accessibility, and connections to pharmacies and other health services are all fundamental variables. In other words, a medical center is not simply a shop with a medical sign; it is an urban node, and its success or failure depends on whether its service radius is feasible.

This also explains why medical property leases are highly valued by the market. Data shows that the weighted average lease term for medical asset classes is typically 7 to 10 years. As medical operations become more corporatized, landlords may face tenants shifting from traditional single clinics to more well-capitalized and mature medical groups or private equity-backed operators. Longer leases, stronger tenants, and more stable cash flow naturally contribute to asset valuation. However, from Dawn's perspective, leases are merely surface-level cash flow; what truly transcends economic cycles is the long-term demand generated by population, transportation, and service networks.

Another shift in healthcare properties is the move from standalone clinics to a healthcare ecosystem. Looking ahead, we should pay attention not only to medical buildings adjacent to hospitals, but also to specialist consulting suites, flexible healthcare room leasing, integrated allied health environments, and the path for healthcare operators to gradually move from tenants to owner-occupied properties. These assets test not only real estate acumen, but also operational logic, space allocation, and service mix. Locations that can connect GPs, radiology, pathology, physiotherapy, mental health, dentistry, pediatrics, and pharmacies often have greater vitality than isolated single clinics.

The changes in NDIS and SDA have made community care space a more worthy subject of study. Data shows that NDIS costs between AU$50 billion and AU$52 billion annually, averaging approximately AU$67,000 per participant. The government aims to gradually reduce the annual increase of approximately 81 TP3T to approximately 21 TP3T. Some lower-demand cases may shift to state government-level projects such as Thriving Kids, leading to increased demand for GP clinics and community care. Regarding SDA, as of June 2025, there will be 11,642 registered SDA residences across Australia, an increase of 231 TP3T compared to June 2024; meanwhile, over 25,000 participants have received SDA funding, and a significant proportion are still seeking suitable accommodation.

The key takeaway from these figures is that the demand for care services hasn't disappeared; rather, it's been redistributed. In the past, the market easily regarded "proximity to hospitals" as the golden rule for care properties, but today's demands place greater emphasis on transportation, amenities, community feel, design quality, and daily convenience. The common language of SDA (Supply, Development, and Services), aged care, community care, and medical centers is "how people are cared for in the city." This is precisely the core proposition of urban planning: property value ultimately returns to people's life paths, not just the name of the use itself.

Queensland is particularly noteworthy in this round of healthcare property trends. Of the approximately AUD 800 million in healthcare facility transactions across Australia between 2024 and 2025, Queensland accounted for AUD 236 million, the highest share nationwide. Prime metropolitan medical assets typically offer initial returns in the high 5% to mid-6% range, while regional products usually offer an additional 50 to 100 basis points. More importantly, during interest rate cycles, medical assets have not weakened as significantly as some office and retail properties, reflecting a certain degree of market acceptance of their defensive nature.

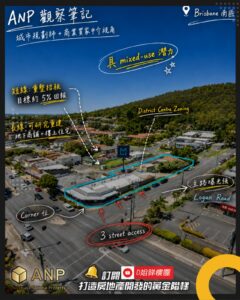

Recent transactions also offer clues. The Maroochy Private Hospital, a $100 million project, features six operating rooms and 45 inpatient beds, covering radiology, orthopaedics, oncology, and research providers, with over 10,000 square meters of leasable space. It already had 951 TP3T pre-leasing prior to opening. Other transactions include the Caloundra medical consulting asset for $8.751 million (5.491 TP3T yield); the Birtinya radiology clinic for $6.4 million (5.541 TP3T yield); the Brisbane Wynnum radiology site for $10.1 million (5.41 TP3T yield); and the Upper Mount Gravatt Logan Road radiology clinic for $5.615 million (5.721 TP3T yield).

Looking only at the yield of these transactions misses the forest for the trees. Dawn would ask deeper questions: Is the location situated in a population growth corridor? Is it close to a catchment area with insufficient medical services? Does it have adequate vehicular traffic, parking, public transportation, and accessibility? Are there already pharmacies, senior communities, residential populations, and allied health services nearby, sufficient to form a medical cluster? Does the land use permit future modifications, expansions, or reorganizations? These questions are the watershed that distinguishes medical properties from "rentable" to "holdable for the long term."

From ANP's perspective, the attention given to healthcare centers is a natural consequence, but investors who only chase trendy labels risk missing the point. Truly high-quality healthcare properties should simultaneously possess population support, accessibility, functional suitability, tenant resilience, service network, and land flexibility. Essentially, they are both commercial properties and community service facilities; they consider both cash flow and urban structure; they must be leasable today and remain a vital part of residents' lives ten years from now.

The 2026 budget brought medical centers into the spotlight, but the bigger story is that Australian cities are reshaping the landscape of healthcare and care services. The most valuable commercial properties of the future will not necessarily be the most visually striking buildings, but rather the spaces best suited to accommodate population changes, community services, and shifts in urban functions.

The attention given to medical centers is merely superficial; what truly deserves study is the underlying urban demand curve.