When many people see Australian land, their first reaction is: "Does buying land mean I'm guaranteed to make a profit?"

Contents Overview

ToggleThe answer is actually:Very different.

Investing in Australian land is not as simple as "buying land and waiting for it to appreciate in value." Different types of land have different zoning, planning restrictions, infrastructure requirements, drainage requirements, street access restrictions, and may even be affected by local government approvals. While they may all appear to be land, the actual implementation can be completely different.

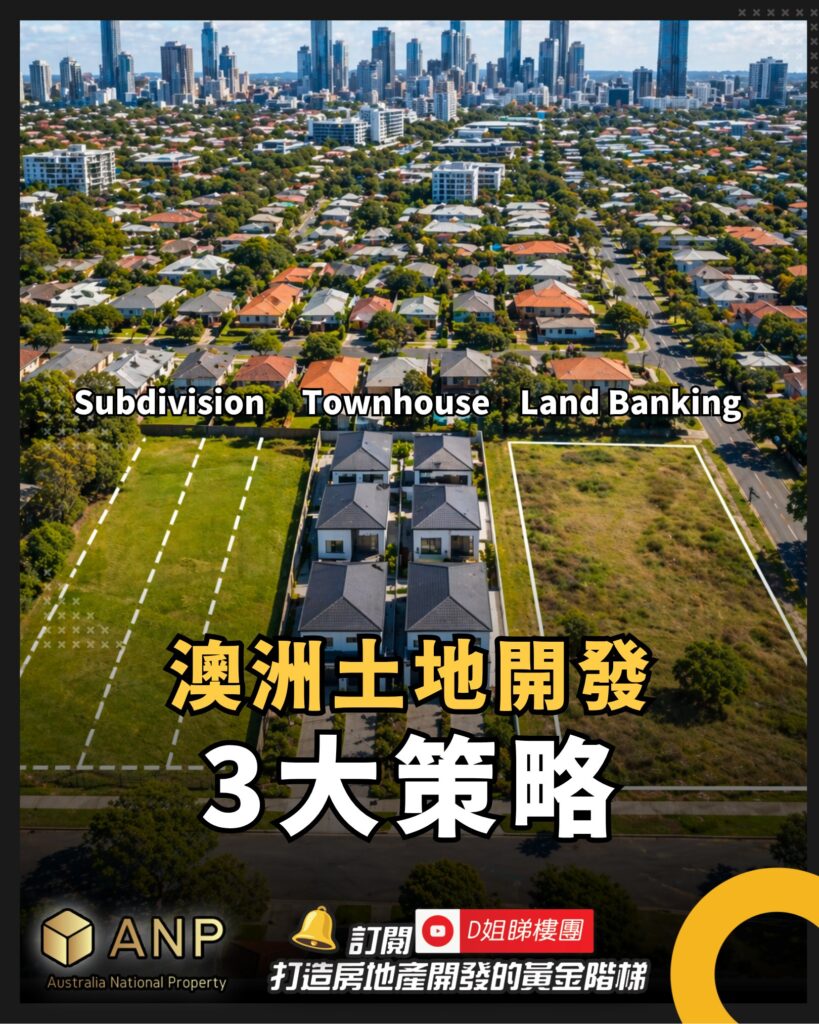

In Australian land development, there are generally three main approaches:

Subdivision, Townhouse, Land Banking.

All three seem to be related to land, but their operating methods, financial pressures, risk tolerance, and return logic are completely different. Before entering the market, the most important question for investors is not "which one is the most profitable," but rather:Which one best suits your funds, time, experience, and risk tolerance?

1. Subdivision: Dividing the land doesn't necessarily mean making money easily.

SubdivisionIn Chinese, this is often called "land division" or "land subdivision." Simply put, it involves dividing a piece of land into two or more plots, which are then sold or developed separately.

For example, a large residential site, if it meets the planning requirements of the local government, may be divided into two separate plots, which can be sold or used to build residential buildings in the future.

This type of investment is usually more like a "planned investment," where the focus is not entirely on the building itself, but on whether the land itself has the conditions for subdivision.

Investors should pay attention to the following:

- Is land zoning permissible to be subdivided?

- Does the land area meet the minimum requirements?

- Are the entrances/exits in all directions reasonable?

- Are connections to drainage, sewage, electricity, and water pipes feasible?

- Do the terrain, slope, and easement affect the planning?

- Does the local government support this type of high-density development?

The advantage of subdivision is that, compared to building multiple townhouses directly, the building management pressure is usually lower, and the capital investment may also be less. However, this does not mean that it is a low-risk project.

Many investors underestimate infrastructure costs, such as reconnecting water and electricity, drainage works, road or driveway design, consulting fees, surveying fees, and council contributions. Once these costs exceed expectations, what initially seemed like substantial profits can be quickly wiped out.

Therefore, the core of subdivision is not "Is this piece of land big enough?", but rather:

Is it really possible to divide this land at a reasonable cost?

II. Townhouse: Offers greater potential for return, but requires the strongest financial resources and execution capabilities.

Townhouse developmentTownhouse development, also known as terraced house development, is a development method familiar to many Australian land investors.

These types of projects typically involve building multiple townhouses on a single plot of land, which are then sold or rented out separately. Compared to simply dividing land, townhouses usually offer greater potential returns because investors don't just profit from the land price difference, but also create higher market value through architecture and product design.

However, the townhouse model also places the greatest demand on execution capabilities among the three.

Because it involves more than just buying land, it also includes:

- Architectural Design

- Planning Approval

- Construction cost control

- Builder Selection

- Project schedule management

- Pre-sale or sales strategy

- Interest costs

- Market price changes

In theory, townhouse development projects can be more profitable; however, in reality, if any one link in the chain goes wrong, the outcome can be completely different.

For example, rising construction costs, construction delays, material shortages, slower-than-expected sales, and even changes in loan terms can all directly impact a project's cash flow.

For investors, townhouse development is not simply about "buying land and building a house," but a complete development business. It requires capital, time, a team, consultants, risk budgeting, and project management capabilities.

Therefore, townhouses are usually best suited not for completely passive investors, but for those who are willing to invest time in understanding the project, take on higher risks, and have the ability to withstand fluctuations in the development cycle.

3. Land Banking: Seems easy, but it actually tests your patience the most.

Land BankingIn Chinese, it can be understood as "land reserves" or "long-term land hoarding".

The core of this strategy is to first purchase land with future development potential, without rushing to develop it immediately, but waiting for population growth, infrastructure completion, planning relaxation, or urban expansion to increase the land value.

For example, some areas located on the outskirts of cities that may be driven by future transportation infrastructure development, population inflows, or planning changes may be considered potential targets for land banking.

It sounds simple: buy, hold, and wait for it to appreciate.

But reality is not necessarily like that.

The biggest challenge in land banking lies in the uncertainty of time. You may be able to judge that a region will develop in the future, but you may not know whether that "future" is three years, five years, or more than ten years.

Investors need to bear:

- Funds are locked up for a long time

- Rental returns may be low

- Carrying costs continue to accumulate

- Interest and property tax pressure

- Policies or zoning may not change as expected.

- Market cycles may not align.

Land banking can sometimes offer substantial returns, but it demands the most patience and macro-level judgment. It's not a tool for short-term doubling of profits, but rather a bet on long-term urban development.

Therefore, this type of strategy is more suitable for investors with longer investment horizons, lower cash flow pressure, and who are willing to wait for the region to mature.

What's the difference between Subdivision, Townhouse, and Land Banking?

Simply put, the differences between the three can be understood as follows:

Subdivision The focus is on planning and partitioning conditions, making it suitable for those who want to reduce building complexity but still hope to create value through land planning.

Townhouse The focus is on development and product value, with high potential returns, but also the greatest pressure in terms of funding, time, and management.

Land Banking The focus is on long-term holding and regional growth. There may be no obvious income or results in the short term, but if the direction is correct, the long-term value may be gradually released.

There is no single best option; the only option is the one that best suits your investment goals.

To gain a deeper understanding of land development opportunities in Australia, ANP can provide relevant information and directional analysis, and can also combine the professional advice of urban planners to assist in assessing land use, planning restrictions, and development potential.